1) MARKET BAROMETER

September surprised everyone. Historically, one of the weakest months, one we often brace ourselves for, turned into one of the strongest. The S&P 500 gained roughly 3.5% in September, while the Nasdaq surged over 5%, posting its best September in more than a

decade. But it is just playing with statistics:-) These gains didn’t arise in isolation. They came on top of a strong year already underway. Through the first nine months of 2025, the S&P 500 had already returned about 14% year-to-date.

Beyond the U.S., the MSCI World 2025 (a global equity index that tracks large and mid-cap stocks from 23 developed countries) has returned modestly,

reflecting a mixed global performance. Meanwhile, gold has been a standout. Its upward run into September bolstered its year-to-date gains (+45% YTD), reinforcing its role as a refuge for cautious capital.

Crypto has remained volatile, with pockets of strength, but no clear consensus across the space. The VIX, meanwhile, has drifted upward during September, whispering of more market stress than the calm surface suggests.

In bond markets, yields continued to rise, particularly for the 10-year U.S. Treasury. That is a headwind for bonds (prices fall as yields rise), and a latent challenge for equities because higher yields effectively raise the bar for future earnings. The rally in stocks is more pronounced when it occurs in the presence of rising yields.

Elsewhere in

global capital flows, India saw about $2.7 billion withdrawn from its equities in September, marking another month of outflows and cooling one of the year’s hottest markets.

Energy prices also climbed, driven by supply concerns and geopolitical tensions, which tightened inflationary stress for many economies.

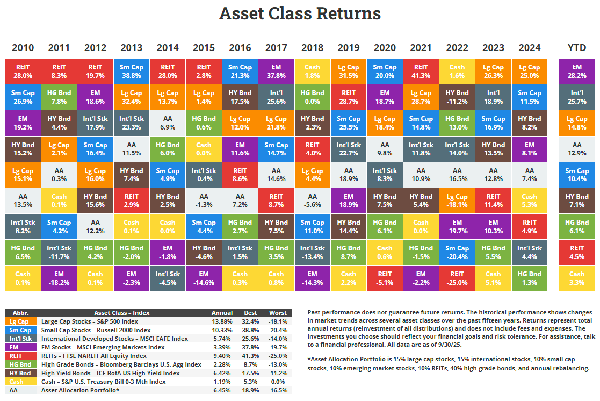

Let´s zoom out and

monitor the performance of different asset classes over the last few years, updated to Q3 2025. It’s a visual reminder that market leadership constantly shifts — what wins one year may lag the next.

So far in 2025, Emerging Markets (+28%) and International Stocks (+25%) have led the pack, while Bonds and REITs have delivered more modest gains.